Japan outlook – Recovery appears set to continue

- 01 December 2022 (7 min read)

Key points

- Japan’s economy looks set to remain robust – we forecast GDP growth of 1.6%, 1.7% and 1.3% in 2022, 2023 and 2024 respectively

- Wage pressures are rising and evidence of firms passing on cost increases are growing

- We expect the BoJ to remain on hold in 2023, but positive shifts in pricing norms could see yield curve control adjusted in 2024

- The next BoJ Governor expected in April 2023 could signal a shift in approach.

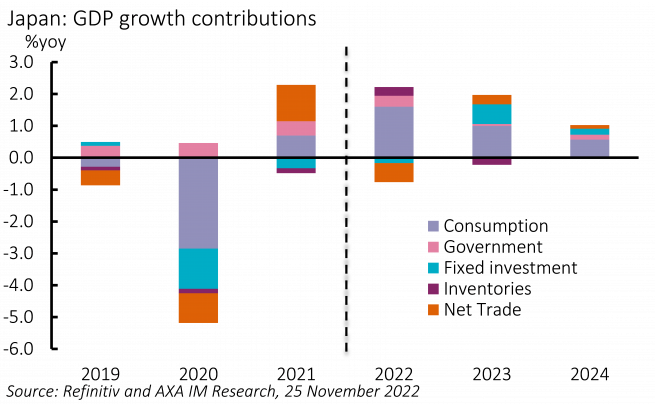

Recovery set to continue

The recovery of the Japanese economy looks set to continue. Growth should be supported by the delayed reopening of the economy from COVID-19 and a recovery in tourism, with the borders of the country now fully open to overseas visitors. The positive growth momentum will be tempered by slowing external demand – we expect recession in Europe and the US and below-trend growth in China in 2023. In 2024 we expect Japan to continue catching up to its pre-pandemic trend (Exhibit 10). We forecast GDP growth of 1.6%, 1.7% and 1.3% in 2022, 2023 and 2024 respectively (consensus 1.5%, 1.3% and 1.1%).

Inflation spike to fade, but price pressures growing

Inflation is set to remain above the Bank of Japan’s (BoJ) target in the near term with a weak yen adding to inflationary pressures. Core Consumer Price Index (CPI) inflation (which excludes only fresh food) is on the rise and likely to peak this quarter. Government intervention is set to cap the increase in inflation in 2023 through additional subsidies on energy. Following this, we expect to see inflation fall in 2024, though companies becoming more willing to pass on price increases to their customers provides some upside risks. We expect CPI inflation to average 2.4% in 2022, 2.1% in 2023 and 1.3% in 2024 (consensus 2.3%, 1.6% and 1.0%). That said, the outlook is for inflation to fall back below the BoJ’s target, with having just risen above target due to extreme external pressure, and far short of elevated inflation across the globe.

Wage dynamics in Japan appear to be improving but do not yet suggest a significant shift in Japan’s pricing norms and spring wage negotiations will be key. Rengo, Japan’s largest Trade Union confederation, confirmed it will request a total pay increase of 5% but final results tend to come in below Rengo’s target – in 2022 Rengo aimed for total pay increase of 4% and achieved 2.2%.

BoJ: The last dove standing

The BoJ continues to emphasise wage growth as a necessary condition to changing its ultra-accommodative policy stance. This has remained the philosophy under Haruhiko Kuroda’s governorship, but things may change following the appointment of a new Governor in April 2023. Deputy Governor Masayoshi Amamiya and ex-Deputy Governor Hiroshi Nakaso are seen as frontrunners. Nakaso is widely seen as more in favour of reducing monetary stimulus and his appointment would raise the risk of a change in policy from Q3 2023 after the spring wage negotiations. We currently still do not expect the 2% inflation target to be achieved in a sustainable manner during our forecast horizon, but we expect the post-Kuroda BoJ to adjust the ultra-accommodative yield curve control (YCC) policy after taking into account recent inflation, shifts in expectations and a gradual rise in wages.

In terms of timing, we believe a decision to change BoJ policy is unlikely before the spring 2023 wage negotiations. But weaker global economic conditions could see the BoJ proceed cautiously and only tweak policy early in the following year when external conditions improve. In addition, we expect the BoJ to wait for clearer evidence that underlying inflationary pressures are growing and to see if core inflation remains above previous levels once the energy shock dissipates. We expect the BoJ to shift the YCC target of around 0% plus or minus 25 basis points (bps) on 10-year Japanese government bond yields to +/-40bps and to make this move in early 2024. Yet this is a finely balanced call and we see risks skewed to the BoJ remaining on hold throughout 2024.

Our views for 2023

Read our full outlook to find out more about our experts' views.

Read our regional outlooks

US outlook – Mild recession to see inflation fall

Eurozone outlook – Difficult roads ahead

UK outlook – Navigating troubled waters

China outlook – A bumpy path to reopening

Emerging markets outlook – Darkest before dawn

Disclaimer

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.