UK outlook – Navigating troubled waters

- 01 December 2022 (7 min read)

Key points

- We expect the UK economy to enter recession this year and forecast GDP growth to average 4.3% in 2022, -0.7% in 2023 and 0.8% in 2024

- Inflation should begin to gradually retrace in 2023, falling towards the BoE’s 2% target in 2024

- Interest rates are likely to peak at 4.25% in Q1 2023, but we expect to see the BoE begin to cut from Q4 and across 2024 to end the year at 3%

- Political developments remain important, in particular the Northern Ireland Protocol negotiations remain a risk.

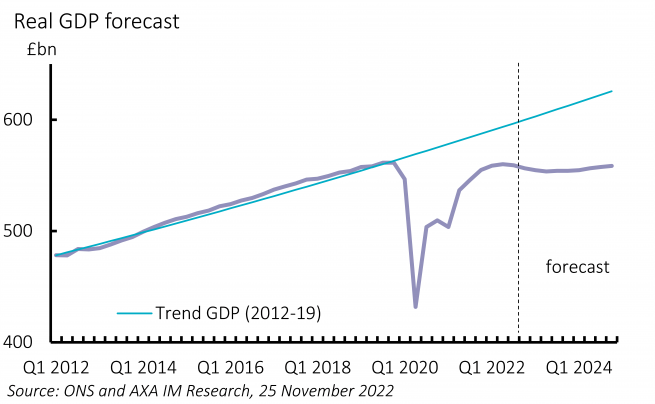

Recession to give way to sluggish recovery

The UK economy has been flashing red for months and the recent decline in Q3 GDP, exacerbated by an additional Bank Holiday, likely marks the beginning of a recession driven by falling consumption, and declines in business and residential investment. We expect this to last around four quarters with a peak-to-trough decline of 1%. Following this, we expect inflation to retrace and alleviate real incomes pressures and for consumption to slowly recover. The slowdown is apparent in levels terms (Exhibit 8) with GDP remaining around its pre-pandemic level. We forecast growth of 4.3% in 2022, -0.7% in 2023 and 0.8% in 2024 (consensus 4.2%, -0.5% and 0.8%).

Labour demand now appears to have turned, lagging declines in economic activity. But a reduction in labour supply has seen unemployment remain low and kept the labour market tight. We see unemployment rising steadily over 2023 and 2024 to peak at 5% towards the end of 2024. We see unemployment averaging 3.6% in 2022, 4.5% in 2023 and 4.9% in 2024.

Energy effects to fade slowly as fiscal stance tightens

Inflation has risen sharply and now stands at 11.1%. We expect a slow decline in the headline rate, with upside contributions from food inflation likely to keep the headline above double digits into 2023. The Government’s decision to extend the energy price cap beyond March next year will help reduce inflation over 2023 as a whole. We forecast Consumer Price Index inflation to average 9.1% in 2022, 7.6% in 2023 and 2.8% in 2024 (consensus 9%, 6.3% and 2.5%).

The Government outlined plans for a sharp fiscal consolidation over the next six years, announcing measures totalling a net £62bn in tightening, despite the impact of energy price caps and recession. This reduces the deficit by £55bn through cuts in spending and increases in taxes. However, energy caps and other cost-of-living top-ups sees the fiscal stance loosen this year, compared to a planned tightening in March. It will now tighten less sharply next year, and the bulk of the tightening now takes place in 2024-2025 and beyond.

BoE first in, first out

The Bank of England (BoE) has increased interest rates by 300 basis points (bps) but the end appears in view. We expect it will increase rates by 50bps in December and February, and 25bps in March to 4.25%. The outlook thereafter, with a growing negative output gap and inflation expected to fall below target towards the end of the forecast horizon, should see the BoE consider loosening policy. We anticipate 25bp cuts in each quarter starting in Q4 2023 bringing rates to 3% by Q4 2024. The precise timing is likely to depend on the scale of labour market adjustment.

Counting down to 2024’s General Election

Negotiations between the European Union and UK on the Northern Ireland (NI) Protocol have resumed as the Government tries to avoid another election in NI. We think second NI Assembly elections by April are likely as the Government seems unlikely to resolve the deadlock. Local elections will also be held in May 2023 but a General Election should be held in 2024. Opinion polls currently suggest a Labour win. However, in contrast to recent elections, both main parties have been forced back to the political centre ground and economic orthodoxy, meaning the next election should be the least economically damaging for a decade.

Our views for 2023

Read our full outlook to find out more about our experts' views.

Read our regional outlooks

US outlook – Mild recession to see inflation fall

Eurozone outlook – Difficult roads ahead

China outlook – A bumpy path to reopening

Japan outlook – Recovery appears set to continue

Emerging markets outlook – Darkest before dawn

Disclaimer

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.