Take Two: ECB keeps rates on hold as inflation dips; markets endure volatility

What do you need to know?

The European Central Bank kept interest rates steady at 2% as Eurozone annual inflation eased to 1.7% in January, from 2.0% the month before. The fall was chiefly driven by lower energy costs, while the core measure, excluding energy, food, alcohol and tobacco, fell to 2.2% from 2.3%. The Bank of England held interest rates at 3.75%, though four of its nine policymakers voted for a 25-basis-point cut. The BoE lowered its UK growth forecast to 0.9% from 1.2% for 2026 and 1.5% from 1.6% for 2027. In contrast, the Reserve Bank of Australia raised rates by 25bp to 3.85%, its first hike in over two years.

Around the world

Markets endured another bout of volatility last week as concerns about the impact of new artificial intelligence offerings on established players and plans for increased AI spending weighed on technology stocks. Over the week to Thursday’s close, the tech-heavy Nasdaq Index was down by 5%, while the MSCI World NR Index fell by 2%*. Gold - often viewed as a so-called ‘safe haven’ during periods of turbulence – also saw its price fall before rebounding over renewed US-Iran tensions and weak US jobs data. Elsewhere, the UK’s blue-chip FTSE 100 index hit a fresh high.

* In US dollar terms. Source: FactSet, data as of 5 February 2026

Figure in focus: 53.0

US business activity expanded in January with stronger output in both its manufacturing and services sectors. The composite Purchasing Managers’ Index rose to 53.0 from 52.7 in December - a reading above 50 indicates expansion. Meanwhile, Japan’s business activity expanded at its quickest pace since May 2023 with its composite PMI rising to 53.1 from 51.1, boosted by higher factory production. However, Eurozone business activity slowed slightly, reaching a four-month low. The bloc’s composite index eased to 51.3 from 51.5 as new orders only rose slightly and employment stagnated.

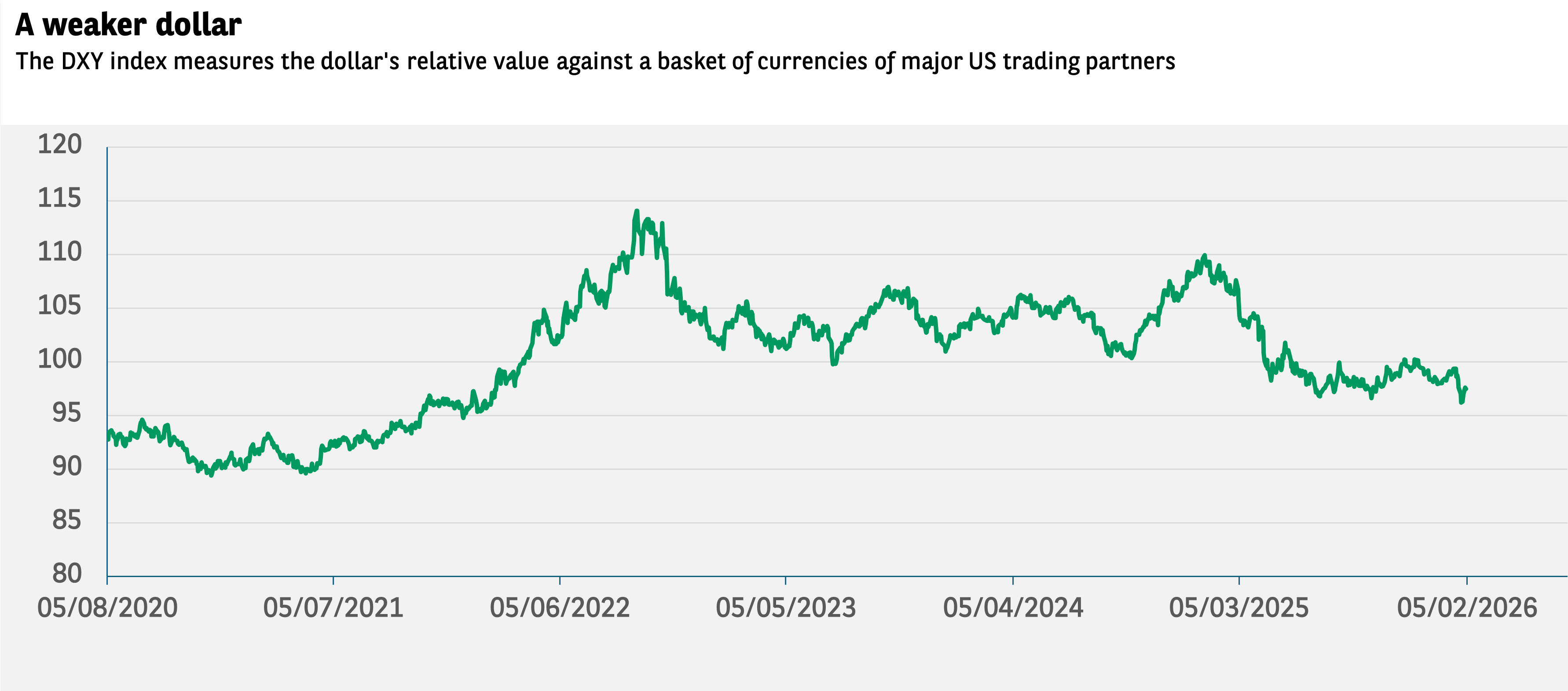

Chart of the week

The US Dollar Index (DXY) plots the greenback’s value against a range of US trade partners’ currencies. The index goes down when the US dollar weakens (i.e. loses value) versus other currencies. It has fallen over 10% in the 12 months through January. Investors have been diversifying away from the dollar partly due to concern over the US government’s economic policies but also to take advantage of opportunities outside the world’s largest economy and further diversify balanced portfolios.

Source: Bloomberg, BNP Paribas Asset Management; February 2026

Words of wisdom

Project Vault: A new US government initiative to create a reserve of critical minerals to protect manufacturers from supply shocks and support US production. The project will initially be funded by the US Export-Import Bank - the country’s official export credit agency - which will provide a $10bn loan, while a further $2bn will come from private capital. The stockpile would include the purchase of rare earths, copper and lithium, as part of an effort to reduce the dependence on China, which dominates the supply chain for many critical minerals. Last week the US, European Union and Japan also announced they intended to work together to make their critical minerals supply chains more resilient.

What’s coming up?

On Wednesday, China issues its latest inflation data, and the US publishes its delayed job numbers update. Thursday sees the UK report a preliminary estimate for fourth quarter GDP growth, while the Eurozone follows on Friday with a second estimate of Q4 GDP. The previous estimate found the Eurozone economy expanded 0.3% in Q4, matching Q3’s growth rate. On Friday, the US publishes its January inflation rate. In December, US annual consumer price inflation rose 2.7%, matching November’s rate.

Read more insights at the Investment Institute

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.