Take Two: Stocks rise ahead of Middle East peace deal

What do you need to know?

Global stocks reached record highs last week in expectation of the US and Iran’s peace deal. The Dow Jones Industrial Average, Euro Stoxx 600 and Nikkei 225 closed at record levels as oil prices fell, and inflation concerns eased. However, while the Federal Reserve held interest rates at 3.50%-3.75% – the first meeting under new Chair Kevin Warsh – it indicated a possible rate hike before the end of this year. Elsewhere, eurozone annual inflation rose to 3.2% in May from 3.0% in April while core inflation, excluding energy, food, alcohol and tobacco, rose to 2.6% from 2.2%.

Around the world

The Bank of Japan raised its benchmark interest rate by 25 basis points to 1% – the highest level since 1995. It said that higher oil prices were passing through to businesses and could increase consumer prices. Japan’s annual inflation rate rose slightly to 1.5% in May from 1.4% in April, data released later in the week showed, while core inflation, excluding fresh food, held steady at 1.4%. Elsewhere, the Bank of England kept interest rates on hold at 3.75%, though two of the nine policymakers voted for a 25-basis-point rise, as UK annual inflation unexpectedly remained unchanged at 2.8% in May.

Figure in focus: 0.6%

China retail sales fell for the first time in over three years, putting pressure on its government to consider fresh stimulus to boost spending. Retail sales fell 0.6% in May from a year earlier – analysts had expected the figure to be flat on the previous month. Urban fixed-asset investment, including real estate, also fell more than expected, underlining continued weakness in the property market.

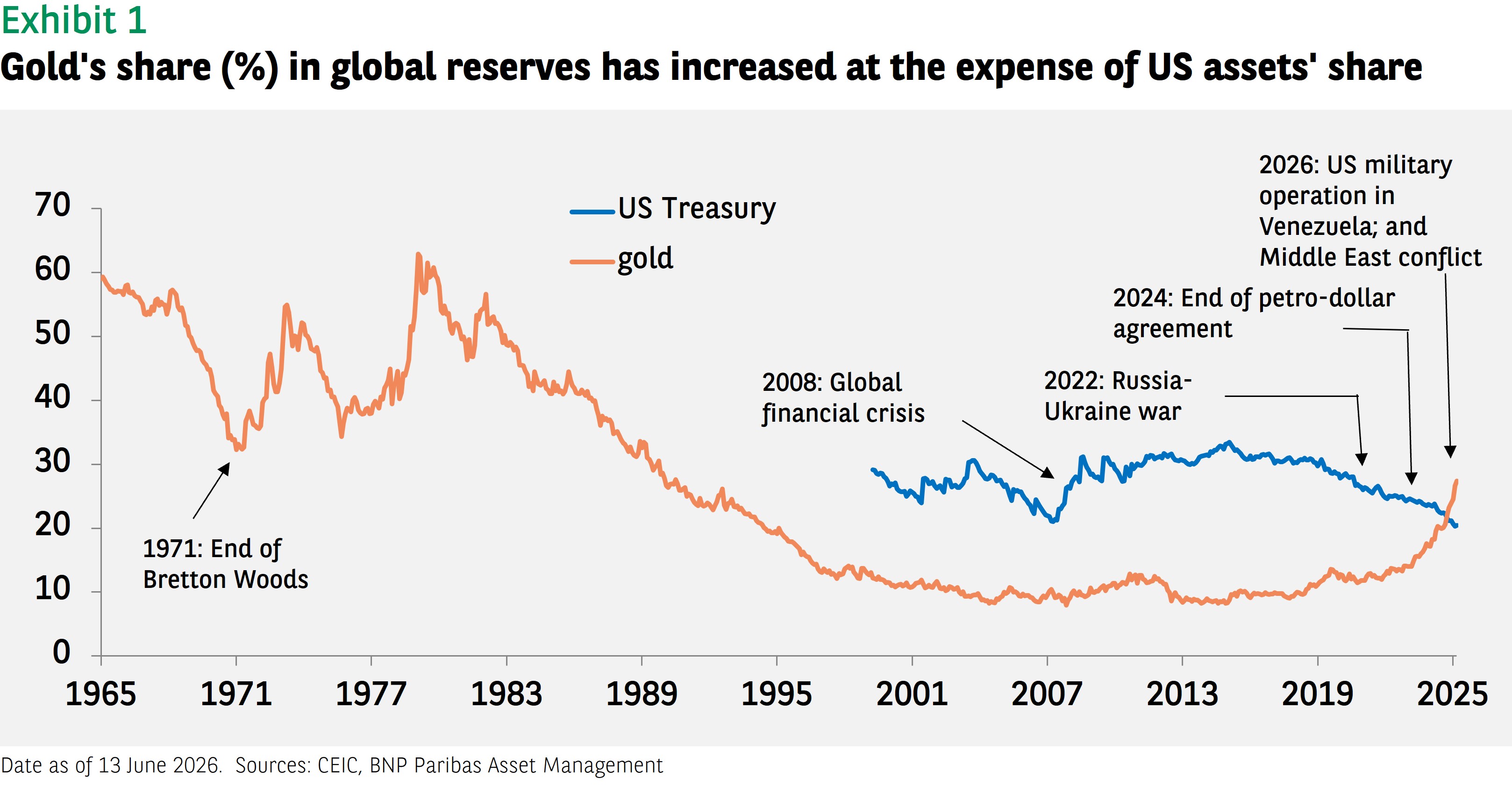

Chart of the week

Many central banks are increasing their gold reserves at the expense of US dollar assets. Investors also tend to trust gold because it is a supranational asset that is not tied to the economic policy or political system of any one country. As a result, the precious metal will likely remain a hedging tool against economic and geopolitical shocks. China has been actively accumulating gold in its foreign reserves and developing its own bullion ecosystem by offering some trading partners who receive renminbi revenues the option of converting some of those proceeds into gold.

Words of wisdom

AMOC: The Atlantic Meridional Overturning Circulation is a system of ocean currents driving warm water north and sending cold water south in the Atlantic Ocean. The AMOC plays a critical role in regulating climate as it transfers carbon dioxide from the atmosphere to the ocean. Recent research suggested the AMOC could weaken much more by the end of this century than previously thought, which could raise sea levels causing flooding, threaten food security and bring colder, harsher winters. However, experts said a lack of data means it is difficult to ascertain the extent to which the AMOC has weakened.

What’s coming up?

On Monday, Canada publishes its latest inflation numbers while Tuesday sees several composite Purchasing Managers’ Indices issued, including those covering Japan, India, the eurozone, US and UK. On Wednesday, Germany posts its closely watched Ifo Business Climate index; the measure rose in May, after falling to a six-year low in April. On Thursday, the US reports its final estimate for first quarter economic growth; the last estimate showed the world’s largest economy had expanded by an annualised rate of 1.6% in Q1, up from 0.5% in Q4.

Read more insights at the Investment Institute

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.