Credit remains attractive in this hightened risk environment

- With bonds now once again delivering higher yields, investors can tap into potentially greater income streams – and we presently prefer up in quality, shorter-duration bonds.

- Extending duration along the curve, to intermediate, offers comparable yield and provides optionality to recognise capital gains once markets start to anticipate central banks easing. Yet our base case is that this is unlikely to occur until 2024.

Buying into a better bond regime, quality counts…

Following the relentless tightening of monetary policy in 2022 all-in yields for investment grade credit have risen materially, on higher government yields and wider credit spreads, placing credit in a positive spotlight. However, the degree and the pace of interest rate hikes was bound to place stress on the financial system adjusted to a low-rate environment. This quarters’ U.S and European bank weakness is one of the signs that higher real and nominal rates are posing financial risks.

Concerns over banking stress contagion have raised renewed questions on forward policy rates and growth. The rally in front-end rates was significant – however, with relatively sticky core inflation, amid strong labour market conditions, the path for policy rates and economic activity is staying uncertain, despite market hopes of monetary relief. As investors wait for the Federal Reserve (Fed) to pause its pace of hiking, bonds offer an opportunity to potentially generate high single-digit returns from high-quality assets – an opportunity that hasn’t presented itself for a long time.

Importantly, the trade-off between risk and reward has improved, with spreads now wider, investors are well placed to benefit from, and harness this higher ‘carry’. US investment grade spreads have risen around 45bps in March, approaching October 2022 levels, getting a 6% yield back on investors asset allocation radar.

Generally, US corporate fundamentals remain resilient and US investment grade companies have managed balance sheets well. Importantly, with economic growth stronger than originally expected, headline inflation easing, and interest rates closer to peak, the pressure on corporate profit margins might not deteriorate significantly from here. Even so, margins are certainly starting from healthy levels.

Some spread volatility is expected due to the slower growth cycle and elevated funding costs, with highly levered issuers likely to find it harder to adjust, particularly companies starting with low interest coverage, and those with unhedged floating rate liabilities. This bodes well with our preference for higher quality credits, with focus on security selection for companies which are more resilient to the slowdown growth cycle. We expect credit selection to remain a key alpha generator, as active managers look for companies with stable earnings, agile operations, and strong liquidity.

… and so, does duration

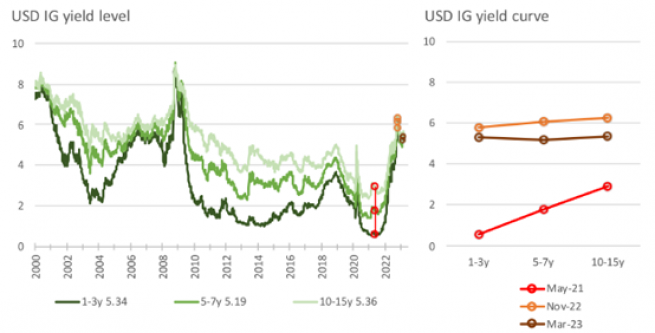

Investors also need to consider the yield term structure of investment grade credit, which is flat, given the inverted shape of the US government bond curve (Illustration 1). As a result, with comparable yields achievable without adding incremental interest rate and credit risks, short-to-intermediate duration strategies offer the possibility of superior risk reward.

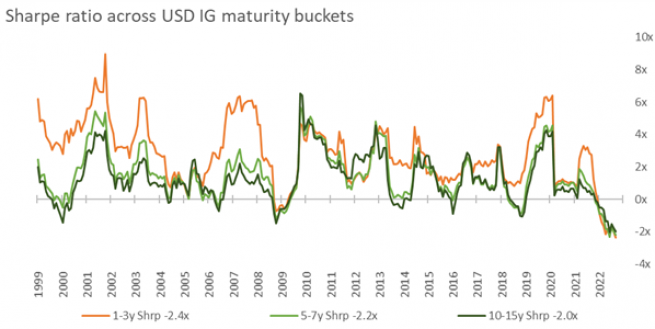

These bonds exhibit lower volatility and have typically generated superior risk-adjusted returns over time (Illustration 2). Specifically, short duration bonds are, in general, less sensitive to rate and credit spread movements compared with debt that has a longer duration. They also offer an ability to boost liquidity – having a larger percentage of an overall portfolio in bonds that mature frequently, creates potential for getting regular cashflows to the portfolio. This might enable investors to avoid forced selling, especially during a stressed economic environment. It should also create a higher reinvestment rate, with the potential to seize investment opportunities in a rising rate environment.

Equally, the price of bonds near its maturity tends to be closer to par than for longer duration bonds. This is due to an ability to estimate coupon and capital payments from short duration bonds with greater certainty than bonds with longer durations – implying lower volatility in returns compared with the broader market. This combination helps eradicate much of the inevitable uncertainty about how markets will move and how central banks will respond.

To harness this opportunity, we advocate staying invested in actively selected, high-quality, shorter maturity bond strategies. For investors with a slightly longer time horizon, intermediate duration bonds can also make a differentiated contribution in a portfolio. In addition to the positive carry available today as coupons have reset at higher levels, intermediate duration bonds will benefit from capital appreciation when the Fed ultimately pivots, and we return to more normal levels of inflation.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.