Take Two: IMF cuts global growth forecast; Eurozone inflation revised up

What do you need to know?

The International Monetary Fund revised down its 2026 global economic growth forecast to 3.1%, from the 3.3% it predicted in January. While the organisation said the Middle East war is threatening to throw growth “off course”, it left its 2027 projection unchanged at 3.2% but warned that a prolonged conflict could slow economic expansion to around 2% this year. However, the IMF added that growth could increase if artificial intelligence-driven productivity gains materialise faster. Elsewhere, global stocks rose on hopes of an end to the Iran war with the S&P 500 breaking through the 7,000 mark for the first time while the Nasdaq and Japan’s Nikkei 225 also reached fresh highs.

Around the world

Eurozone inflation rose to 2.6% in March, up from 1.9% in February and above the preliminary estimate of 2.5%. The increase largely reflected a surge in energy prices on the back of the Iran conflict. Inflation now stands at its highest level since July 2024, and above the European Central Bank’s 2% target for the first time this year. Core inflation, excluding energy, food, alcohol and tobacco, eased to 2.3% in March, from 2.4% in February. Eurozone inflation is expected to average 2.6% through 2026 according to the ECB’s latest forecast.

Figure in focus: 5%

China’s economy grew 5% in the first quarter of 2026, beating analyst estimates of 4.8%, and up from 4.5% in the previous quarter. Stronger exports and manufacturing helped drive growth, offsetting sluggish domestic consumption and falling property investment. China recently lowered its annual growth target to a range of 4.5% to 5%, from a previous target of “around 5%”, its lowest goal since 1991. Separately, China’s trade surplus reached its lowest level in over a year in March as export growth slowed to 2.5%. Meanwhile China’s imports surged 27.8%, marking their strongest growth in more than four years.

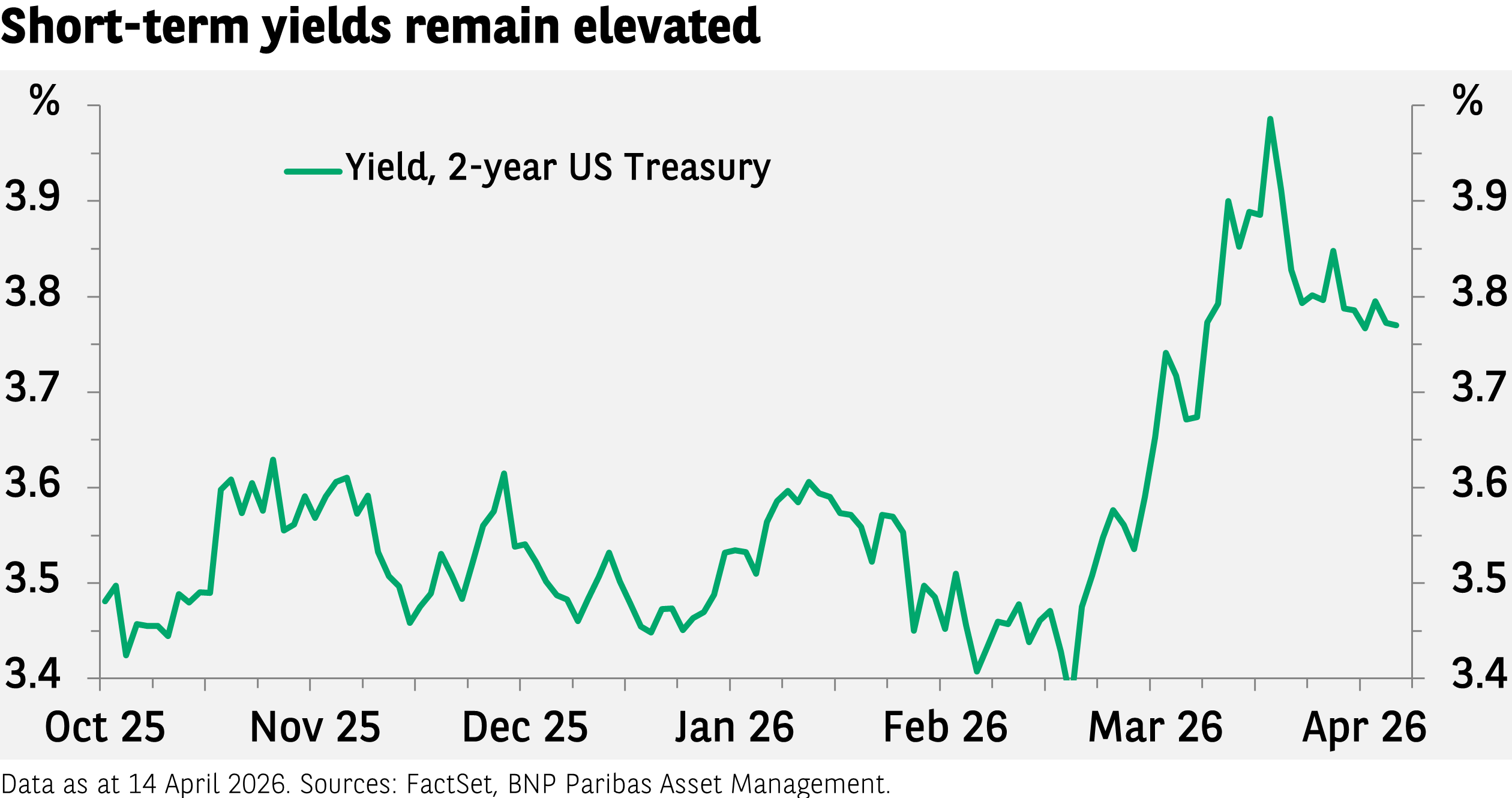

Chart of the week

Equity markets have recovered strongly since a two-week ceasefire in the Middle East was announced. Short-dated bond yields have, however, remained high - two-year US Treasury yields are still close to 3.80%. Short-term bond yields are driven by expectations of future central bank interest rate policy. Higher energy prices and the inflation shock have put an end to hopes of looser US monetary policy in 2026. Financial conditions are tightening, which makes things tougher for US consumers and corporates.

Words of wisdom

Super El Niño: An unusually strong climate pattern that could cause extreme weather events and push global temperatures to record levels next year. El Niño is the warming phase of sea temperatures in the tropical Pacific Ocean - a naturally occurring climate pattern, whose counterpart is La Niña, the cooling phase. Where a standard El Niño phase is defined by sea surface temperatures rising at least 0.5°C above the long-term average, a ‘super El Niño’ phase is marked by a rise of at least 2°C – which according to reports has only occurred a few times since 1950.

What’s coming up?

Canada updates markets with its latest inflation data on Monday. On Tuesday the Eurozone’s ZEW Economic Sentiment Index is published while the UK reports unemployment figures and follows with inflation data on Wednesday. Thursday sees several flash Purchasing Managers’ Indices published, including those covering the US, Eurozone, UK and Japan. On Friday, Japan releases inflation data while Germany issues its closely watched Ifo Business Climate index.

Read more insights at the Investment Institute

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.