Take Two: Middle East ceasefire lifts stocks; US GDP growth revised down

What do you need to know?

Global stock markets rose last week after a two-week ceasefire between the US and Iran was announced. On the back of the news, oil prices eased back while share prices and bond markets rallied. But market confidence remains fragile, especially as Israel carried out military strikes on Lebanon during the week. Over the week to Thursday’s close, the MSCI World NR, S&P 500 and MSCI Europe indices each rose by 4%, while Japan’s Nikkei and the UK’s FTSE All Share were ahead by 7% and 3% respectively.*

*In US dollar terms. Source: FactSet, data as of 9 April 2026

Around the world

US interest rates could rise if inflation remains higher for longer due to the Middle East conflict, but equally a prolonged war could lead to labour market softening, warranting rate cuts, according to the Federal Reserve’s latest meeting minutes. Overall, policymakers felt it was “too early to know” the effect the conflict would have and voted to leave interest rates on hold at 3.5%-3.75% at its March meeting. Separately, US economic growth was revised down to 0.5% (annualised) for the fourth quarter of 2025, from a previous estimate of 0.7% and compared to Q3’s 4.4% rate. The government shutdown was the primary cause of the lower GDP numbers for Q4.

Figure in focus: 50.7

Eurozone business activity slowed to a nine-month low in March as cost pressures intensified. The composite Purchasing Managers’ Index fell to 50.7 from 51.9 in February - a reading above 50 indicates expansion. However, the reading was slightly better than the flash estimate of 50.5. Demand weakened, reflecting a drop in new orders in the service sector, though manufacturing output remained solid, data provider S&P said. Elsewhere, UK business activity expanded at the slowest pace in six months in March. The composite PMI fell to 50.3 from 53.7 the month before.

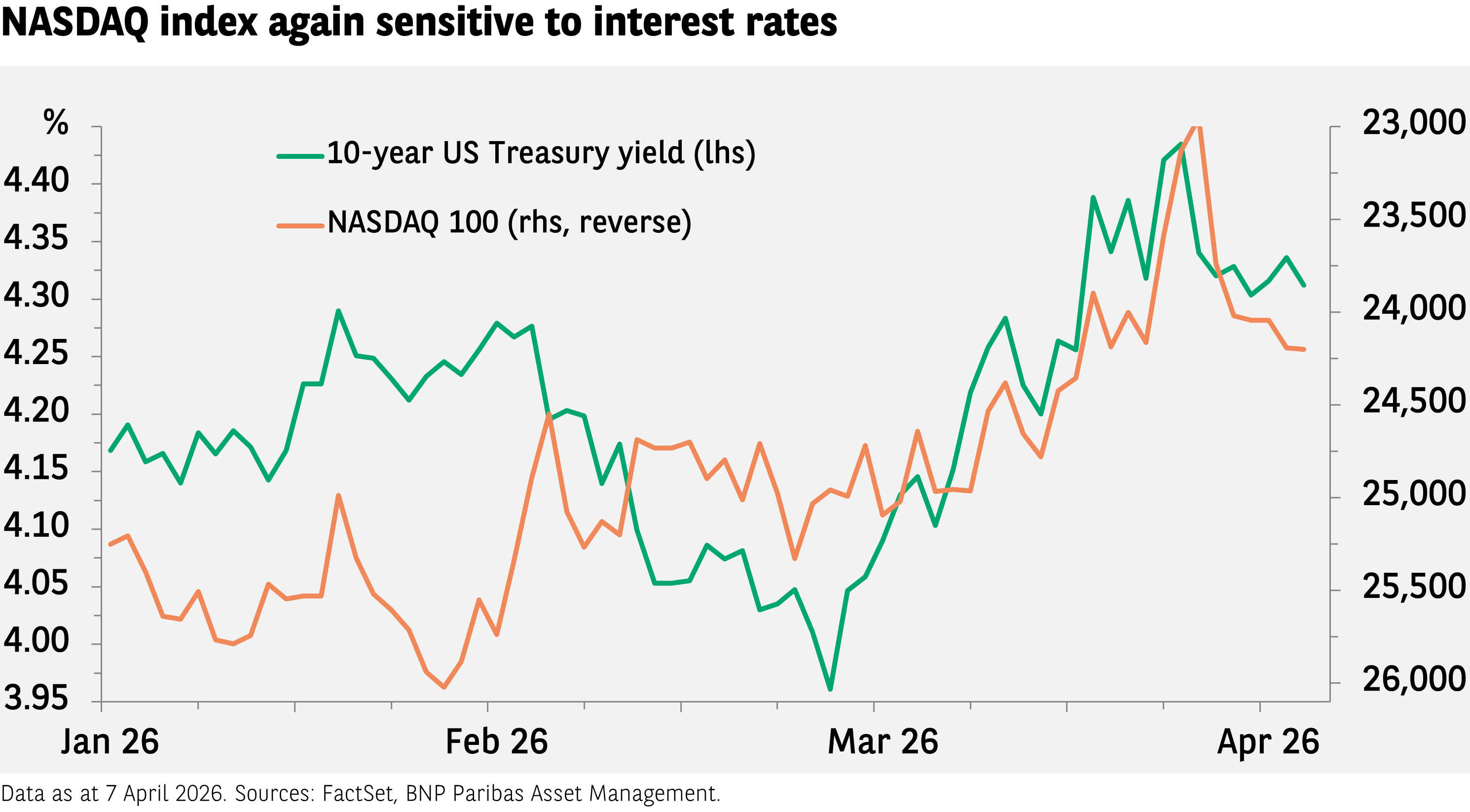

Chart of the week

Corporate earnings are, of course, critical to the performance of technology stocks, but valuations also matter, and here interest rates play an important role. This was evident in 2022 when interest rates rose on the back of post-pandemic inflation, and the Nasdaq 100 fell sharply. Until recently, the technology-heavy index moved primarily based on the perceived impact on earnings from developments in artificial intelligence. Lately, as interest rates rose alongside inflation worries, the Nasdaq fell. If the situation in the Middle East continues to improve, interest rates could move back down, which should support the index.

Words of wisdom: Smile

China and Europe are teaming up for a joint space project that aims to understand solar turbulence and predict geomagnetic storms that can disrupt communications systems and damage electronic equipment. The satellite - the Solar wind Magnetosphere lonosphere Link Explorer, or ‘Smile’ - will capture images and videos of what happens when solar winds come into contact with the Earth’s magnetic field as well as allowing scientists to observe the full Sun-Earth connection for the first time. The data could allow scientists to better forecast weather in space and predict storms that affect the planet, to help prepare for power failures and reduce the impact on infrastructure and communities.

What's coming up?

The International Monetary Fund and World Bank’s Spring Meetings begin on Monday and run until Saturday. In terms of economic data updates, Tuesday sees China issue import and export figures for March, while the US publishes its Producer Price Index measure of inflation. On Wednesday the Eurozone issues industrial production numbers. China publishes its Q1 GDP growth rate on Thursday when the Eurozone also issues its final inflation rate estimate for March.

Read more insights at the Investment Institute

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.