Take two: Oil price climbs amid Middle East conflict; Japan GDP revised up

What do you need to know?

The price of Brent crude oil surpassed $100 a barrel for the first time in almost four years last week, driving further market volatility. The spike prompted the International Energy Agency – the global energy watchdog – to announce the largest-ever release of emergency oil stocks. It said its 32 member countries had agreed to make around 400 million barrels of oil available to the global market, to shore up supply amid the ongoing Middle East conflict. Over the week to Thursday’s close, the MSCI World NR and the S&P 500 were each down by 2%, while the MSCI Europe index fell by 1%.*

*In US dollar terms. Source: FactSet, data as of 12 March 2026

Around the world

US annual inflation remained unchanged at 2.4% in February, matching January’s rate as rising food and housing costs were offset by falling prices in other sectors. Core inflation, excluding more volatile energy and food prices, also remained unchanged at 2.5%. Meanwhile, China’s inflation rate rose to 1.3% in February from 0.2% in January, its highest level in three years, driven by higher spending over the Lunar New Year holiday period. Separately, China exports jumped by 21.8% in the first two months of this year, despite ongoing trade tensions with the US, driven by strong demand for electronics.

Figure in focus: 1.3%

Japan’s economy grew by more than originally estimated in the fourth quarter of 2025, after business investment and private consumption were revised up. GDP growth was raised to 1.3% from the 0.2% earlier reported, following a 2.6% contraction in Q3. However, separate data showed household spending – which accounts for more than half of Japan’s economy - unexpectedly fell in January. Given the backdrop of geopolitical uncertainty and high oil prices, which could impact inflation and consumer spending, the Bank of Japan is expected to keep interest rates on hold when it meets this week.

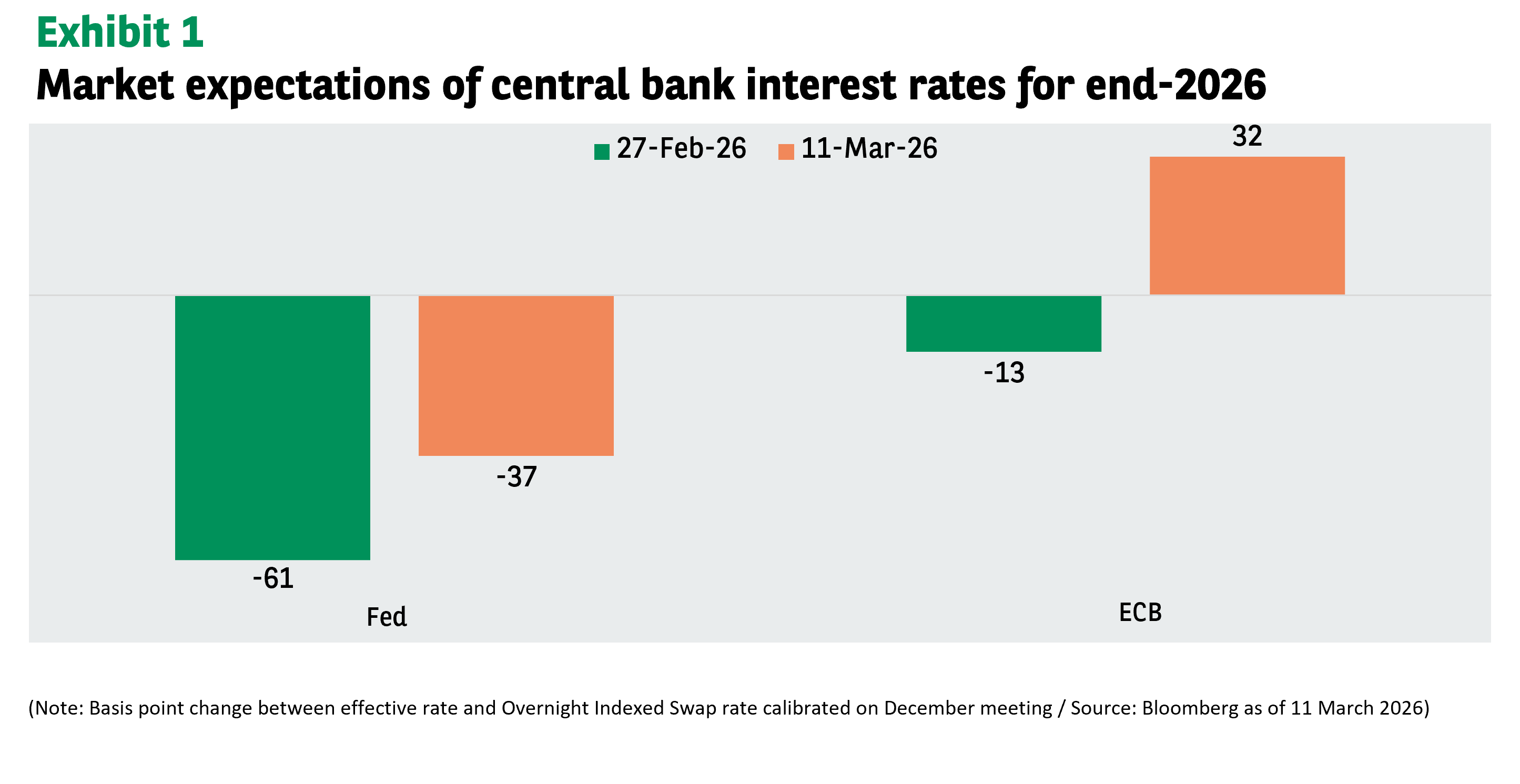

Chart of the week

The Middle East conflict is having a significant effect on monetary policy expectations. Prior to the start of the current military action, the market was anticipating the Federal Reserve would make more than two 25-basis-point interest rate cuts this year, while the European Central Bank would ease by around 13bp, based on market pricing. But these expectations have changed to just 37bp of cuts by the Fed and to over 30bp of hikes by the ECB. The main issue is inflation - the longer the oil market remains subject to geopolitical risk, the more likely it is that there will be a monetary policy reaction.

Words of wisdom

Ocean alkalinity enhancement: Ocean alkalinity enhancement is a method that scientists are exploring to potentially help mitigate ocean acidification and climate change. It involves adding alkaline chemicals to the ocean in an effort to increase its ability to absorb carbon. On a large enough scale, and when combined with emissions reductions, this could potentially help to limit global warming from exceeding 2°C above pre-industrial levels, according to reports. A recent scientific trial showed encouraging results, with no measurable negative impact on the ocean ecosystem, but more extensive tests as well as greater investment are needed if it is to be scaled up in a meaningful way.

What’s coming up?

Monetary policy is in focus this week. The Reserve Bank of Australia meets on Tuesday to set interest rates, while Wednesday sees the Bank of Canada and the Fed convene for their respective monetary policy meetings. The Bank of Japan, Bank of England and the European Central Bank hold their own rate-setting meetings on Thursday. In terms of economic updates, Canada issues its latest inflation data on Monday. On Tuesday, the Eurozone publishes its ZEW Economic Sentiment index followed by inflation data on Wednesday, when the US also publishes its Producer Price Index measure of inflation.

Read more insights at the Investment Institute

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.