How the pandemic has given a new meaning to ageing

- 24 July 2021 (5 min read)

This content was paid for and produced by AXA IM in partnership with the Commercial Department of the Financial Times

The silver economy is no longer just being driven by the over-65s

Within the next 20 years, the number of people in the UK aged 65 and over is set to increase 40 per cent.1 In the US, Europe and Japan, it is a similar story: people around the world are living longer than ever before.

Until recently, the business opportunities surrounding longevity were associated first and foremost with the silver economy — the 750m people aged 65 and over that comprise one of the biggest spending cohorts of any age group. But the prospect of living longer heralds profound changes in the health and lifestyle choices for adults young and old.

“Peter Hughes, Lead Portfolio Manager of AXA Investment Managers' (AXA IM) Longevity Economy strategy, says: “The important thing about the longevity economy is that we talk very much in terms of whole life, not end of life. If you are going to live to be 100, you have to stay fit and active throughout your entire life.”

Longer and healthier living

Ageing and lifestyle forms one of five long-term secular themes identified by AXA IM that stands to drive growth within the evolving economy over the next decade and beyond. While the global population aged 60 and over is expected to reach 1.4bn by 2030, and account for 55 per cent of global wealth, generations of all age groups are spending increasing amounts of their disposable income on living healthier lifestyles.2

The implications for businesses that cater to this rising demand were already making themselves felt prior to the pandemic. But the outbreak of Covid-19 has accelerated and deepened those trends.

- XSBPZmZpY2Ugb2YgTmF0aW9uYWwgU3RhdGlzdGljcywgMjAxNywgcHJpbmNpcGFsIHByb2plY3Rpb24sIFVLIHBvcHVsYXRpb24gaW4gYWdlIGdyb3VwcywgRGVjZW1iZXIgMjAxNw==

- IE1jS2luc2V5IEdsb2JhbCBJbnN0aXR1dGUsIEFwcmlsIDIwMTY=

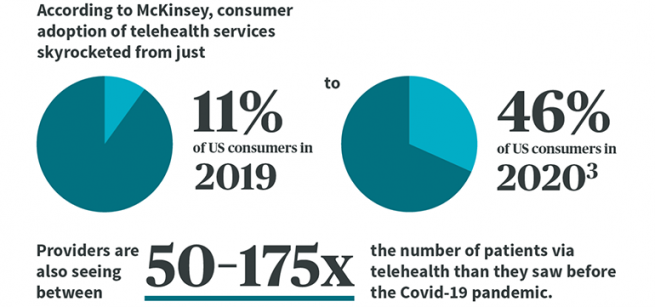

The surge in demand for virtual care has even sparked a new wave of corporate deal making: in August last year, Teladoc Health, a virtual care company, agreed to buy rival Livongo in a $18.5bn cash-and-stock deal as part of plans to capitalise on the spike in demand for remote healthcare services.*

Hughes says: “We’ve seen a growth in digital applications and innovations that have come out of the pandemic because people are now actually getting their healthcare at home.”

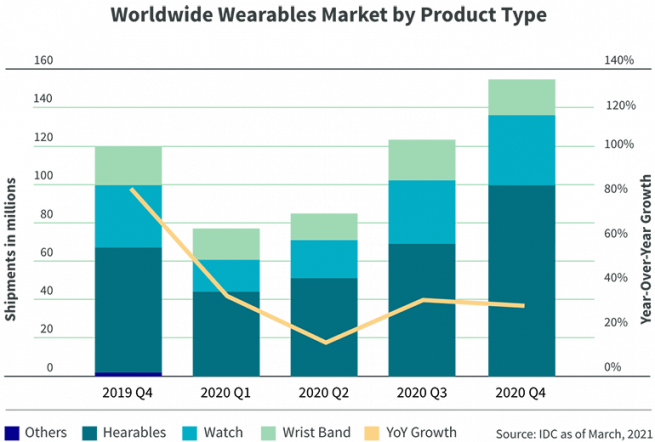

As part of the wider effects of living longer, and spurred by the pandemic, the wearables market has exploded. According to the International Data Corporation (IDC), the global wearables market grew 27 per cent during the fourth quarter of 2020, compared with the same period the year before. The IDC forecasts shipment volumes of wearable devices to grow around 12 per cent every year between now and 2024.

Health and life insurance companies are increasingly turning to wearable technology to tackle obesity and to encourage their clients to become healthier, offering them financial incentives that also reduce costs for the insurer.

The prevalence of obesity in the US has risen steadily since the 1960s, increasing from 3.4 per cent of adults in 1962 to 39.8 per cent in 2016, according to a 2018 report by the Milken Institute3 . The same report estimated that chronic diseases driven by the risk factor of obesity and being overweight in the US accounted for $480.7bn in direct healthcare costs in 2016.

Education to last a lifetime

Living longer is set to affect consumption patterns in less obvious areas. One of them is an increase in demand for learning, in particular because longer lives imply a greater need for retraining and reskilling. “Education will play a critical part of the longevity economy because not only will technology make some jobs obsolete, but people are going to have much longer middle parts of life, where retirement will be shifted to later, making way for multi-staged careers that can span 30-40 years which require retraining or re-skilling," says Hughes.

Duolingo, an artificial intelligence-driven language app, saw the number of new users double in March last year just as the pandemic took hold. The biggest surge came during the week of March 16 after the World Health Organization declared a global pandemic.4

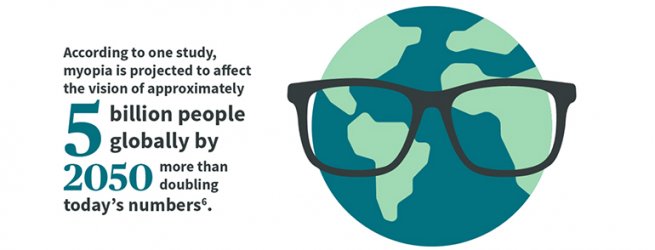

Another emerging area of opportunity from living longer in the digital era is eyecare. The dramatic increase in the use of screens in work and education due to the pandemic has aggravated the growing problem of myopia.

- QW1lcmljYSdzIE9iZXNpdHkgQ3Jpc2lzOiBUaGUgaGVhbHRoIGFuZCBlY29ub21pYyBjb3N0cyBvZiBleGNlc3Mgd2VpZ2h0LCBNaWxrZW4gSW5zdGl0dXRlLCBTZXB0ZW1iZXIgMjAyMA==

- Q2hhbmdlcyBpbiBEdW9saW5nbyB1c2FnZSBkdXJpbmcgdGhlIENPVklELTE5IHBhbmRlbWljLCBEdW9saW5nbywgQXByaWwgMjAyMA==

In response, US-based CooperVision, which specialises in contact lenses, and Essilor of France, which produces lenses, this year formed a joint venture called SightGlass Vision to accelerate the commercialisation of spectacles designed to reduce the progression of myopia in children.*

Many of today’s changes in lifestyle have become far more visible because of Covid-19. But with longevity now a long-term structural theme, their effects will be felt for years after the virus has been contained.

“There are a lot of takeaways from Covid-19 that will manifest themselves in terms of the shift to a healthier life,” says Hughes. “And many things that, at face value, are targeted at older generations are going to be universally beneficial and universally in demand.”

For investors, all of this presents a deep, structural change that creates longevity-linked opportunities stretching far beyond the silver economy.

Investment involves risks, including the loss of capital. This material does not contain sufficient information to support an investment decision.

Disclaimer

*All companies or stocks mentioned are for illustrative purposes only and should not be considered as advice or a recommendation for an investment strategy.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

In other jurisdictions, issued by AXA Investment Managers SA’s affiliates in those countries.

Disclaimer

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.